Learn how we are working to transform how we use and produce energy.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

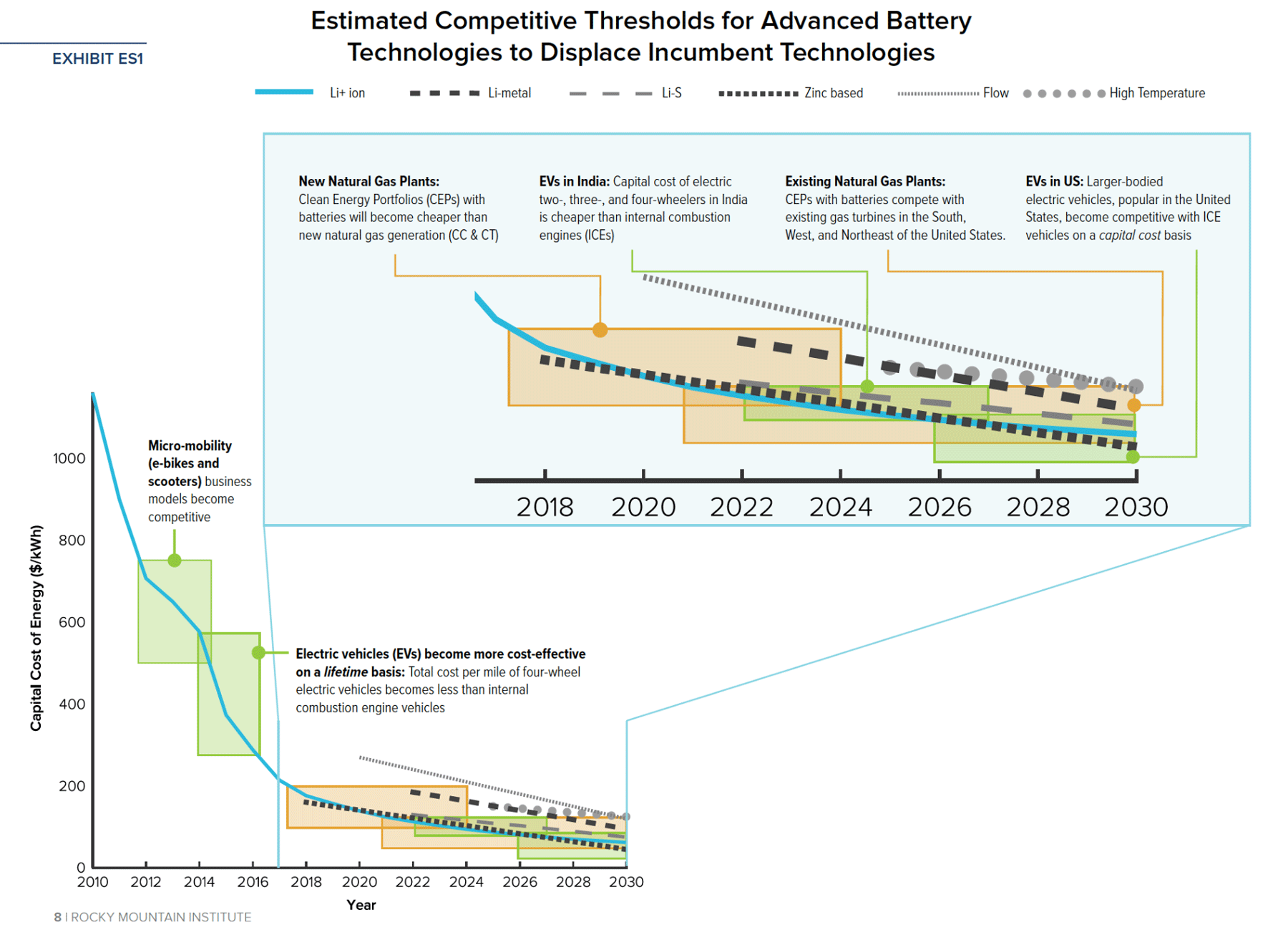

Rapid advancements in battery technology are poised to accelerate the pace of the global energy transition and play a major role in addressing the climate crisis. With more than $1.4 billion invested in battery technologies in the first half of 2019 alone, massive investments in battery manufacturing and steady advances in technology have set in motion a seismic shift in how we will organize energy systems as early as 2030.

According to evidence detailed in RMI’s Breakthrough Batteries Report, cost and performance improvements are quickly outpacing forecasts, as increased demand for electric vehicles (EVs), grid-tied storage, and other emerging applications further fuels the cycle of investment and cost declines and sets the stage for mass adoption.

Total manufacturing investment, both previous and planned until 2023, represents around $150 billion dollars, and analysts expect the capital cost for new planned battery manufacturing capacity to drop by more than half from 2018 to 2023. This is opening new markets—as performance and costs improve—and will push both lithium-ion (Li-ion) and new battery technologies across competitive thresholds faster than anticipated.

The report illustrates how diversifying applications will create opportunities for new battery chemistries to compete with Li-ion, including: solid state batteries, such as rechargeable zinc alkaline, Li-metal, and Li-sulfur that will help electrify heavier mobility applications; low-cost and long-duration batteries, such as zinc-based, flow, and high-temperature technologies that will be well suited to provide grid balancing in a high-renewable and EV future; and high-power batteries, which are well positioned to enable high penetration and fast charging of EVs.

As the battery market continues to grow, battery technology will contribute to the replacement of natural gas plants and gain a foothold in other new market segments, including heavy trucking and short-range aviation. With this transition, legacy infrastructure across the fossil fuel value chain risks becoming stranded, including gas pipelines and internal combustion engine manufacturing plants. Already, battery cost declines are contributing to cancellations of planned natural gas power generation.

What This Means for Industry Players

The report examines how an increasingly electrified, Li-ion battery-dominated world in the near term will open, in the longer term, significant new market opportunities for other emerging battery technologies that are nearing commercial readiness. RMI’s analysis of emerging battery technologies identified six categories (in addition to advanced Li-ion) with significant potential for achieving commercial production by 2025. The below figure shows companies’ anticipated technology commercialization timelines.

RMI’s analysis identifies the implications of these breakthrough battery technologies for investors, regulators, policymakers, and other energy industry players, and identifies risk mitigation and investment strategies that can reduce potential stranded asset risks. It outlines strategies to encourage faster adoption and globally scaled manufacturing of innovative battery and storage technology ecosystems.

It is clear that breakthrough battery technologies will play a central role in our energy system sooner than previously thought possible, creating diverse opportunities for value creation and capture in the transition to a clean energy economy. But capturing the vast potential requires a holistic approach from public and private sectors alike. Collaborative, systems-based strategies to developing battery-enabled markets will provide an opportunity to hasten the rapid and economic transition to resilient, clean, and affordable energy systems.

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.